Bundeshaushaltsmonitor 2026

Unsere Analyse zeigt, dass restriktive Geldpolitik den Ausbau erneuerbarer Energien verteuert.

Unsere Analyse zeigt, dass restriktive Geldpolitik den Ausbau erneuerbarer Energien verteuert.

Der Schwerpunkt der Wohnraumförderung hat sich von Objekt- zu Subjektförderung verschoben. Damit hat sich die Wohnungspolitik in eine teure Zwickmühle manövriert.

Unsere Analyse zeigt, dass restriktive Geldpolitik den Ausbau erneuerbarer Energien verteuert.

Die Ursachen für sinkende Bildungsqualität liegt in zersplitterten Finanzstrukturen und die größten Finanzbedarfe liegen bei den Kommunen.

Analyse der BEG-Verteilungswirkung: Warum Investitionsförderung Härtefälle verfehlt und wie der Sanierungskostendeckel Spitzenbelastungen kostenneutral abfedert.

Europe holds more cards than assumed: chokepoints in uranium enrichment and turbine supply, a USD 10 trillion consumer market US tech cannot abandon, and a coming LNG buyer’s market

Eine Sozialstaatsreform wie von der Kommission vorgeschlagen, die Bürgergeld, Wohngeld und Kinderzuschlag in einer Leistung zusammenfasst und die geltenden Hinzuverdienstregeln reformiert, kann den Bundeshaushalt entlasten.

Der Bund gibt jährlich 60 Milliarden Euro für Subventionen an Unternehmen aus. Wir entwickeln einen Kosten-Nutzen-Indikator zur Bewertung dieser Subventionen: die Fiskalische Kosten-Arbeitsplatz-Relation (FisKAR).

In den 2000er Jahren war Deutschland Exportweltmeister, mittlerweile fällt es zurück. Kann ein Turnaround gelingen?

Bs 2045 müssen deutsche Energieversorgungsunternehmen nominal rund 627 Milliarden Euro in Stromverteil-, Gasverteil- und Wärmenetze investieren. Dazu braucht es einen zusätzlichen Eigenkapitalbedarf bis 2045 von 63 Milliarden Euro.

Für ein zukunftsfähiges Verkehrssystem ermittelt diese Studie einen öffentlichen Investitionsbedarf von mindestens 390 Milliarden Euro bis 2030 und 435 Milliarden Euro für die Folgejahre bis 2035. Dieser Bedarf entfällt überwiegend auf den Bund; ein relevanter Anteil ist unter aktuellen Finanzierungszusagen noch nicht verlässlich finanziert. Neue bzw. ausgeweitete Finanzquellen sind nötig, um die Bedarfe zu decken. Die Studie beschreibt fünf Finanzierungsoptionen (Steuern, staatliche Kreditaufnahme, Nutzungsgebühren, privates Kapital und im ÖPNV Beiträge für Nutznießende), ihre Vor- und Nachteile sowie Zielkonflikte und skizziert eine beispielhafte Finanzierungslösung.Die Studie wurde begleitet vom Sachverständigenrat für die Finanzierung eines zukunftsfähigen Verkehrssystems. Der Rat unterstreicht, dass Auswahl und Gewichtung der Finanzquellen eine drängende politische Aufgabe ist und gibt acht konkrete Empfehlungen ab.

The method used to estimate potential output largely determines the fiscal space available to the EU and its Member States.

Wir untersuchen, ob eine stärkere Internationalisierung des Euro wünschenswert wäre.

Eine pauschale Verlängerung der Zuschüsse über 2026 hinaus ist kritisch zu hinterfragen.

Germany’s federal budget could lose all disposable fiscal space within ten years, a new indicator warns. Without reforms to the budget and the debt brake, and without bringing more people into the labor market, future governments will have no room to maneuver.

The ECB’s strategy is under review, and rightly so. Recent inflation shocks have exposed weaknesses in the ECB’s current approach. It focuses too narrowly on medi-um-term inflation expectations and relies almost exclusively on interest rate adjust-ments.

In this paper, we show that DSAs currently largely ignore economic impacts resulting from climate damages, as well as from the climate policies needed to satisfy the emissions constraint set by European climate targets.

The US semiconductor company Intel is planning to build two ultra-modern chip factories near Magdeburg. This project was promised the largest industrial policy subsidy that the German government has ever approved for an individual company: almost 10 billion eu-ros. Is this money well-spent? To answer this question, we developed guidelines for the evaluation of government investments (BESTInvest). This paper sets out these guidelines and applies them to Intel-Magdeburg. Our conclusion is that the subsidy is controversial.

Strengthening Europe’s sovereignty has become a much-debated policy goal. This paper adds three arguments to ongoing discussions.

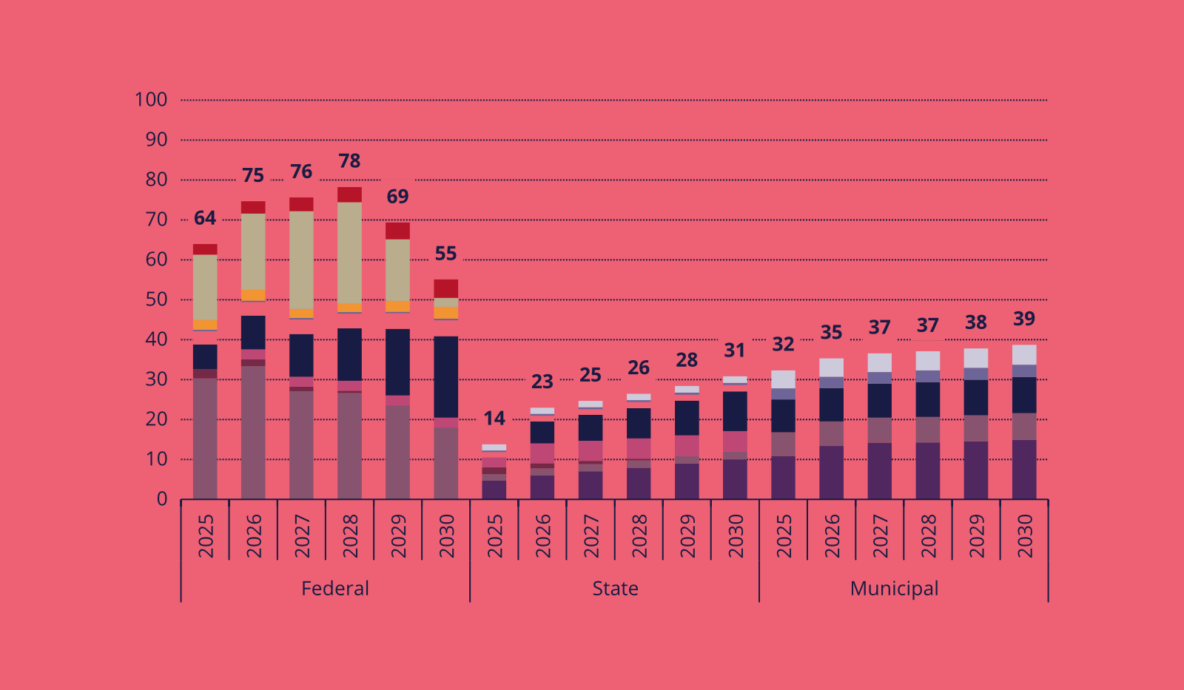

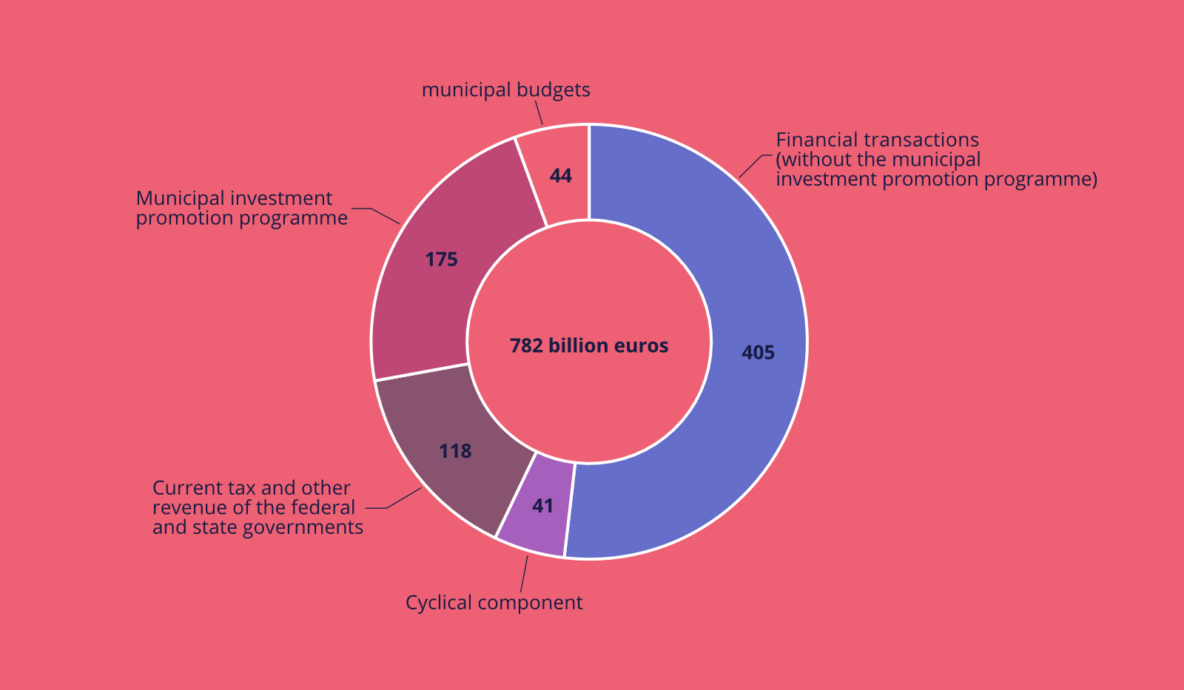

This study maps the additional public financing needed to achieve widely accepted targets in areas that are pivotal to Germany’s stability and future. Overall, we estimate an additional public financing need of 782 billion euros across all levels of government from 2025 to 2030. This would correspond to an average of around 3 percent of gross domestic product (GDP) per year. Our findings are consistent with and complement other estimates of public needs published this year. The need for significant additional public financing for the future viability and modernization of the country can thus increasingly be seen as a consensus position.

Germany needs 782 billion euros in additional public spending for its modernisation by 2030. German politicians have so far lacked a reliable financing framework for this purpose; there are constant discussions around spending cuts or a constitutional reform of the debt brake. Neither strategy can realistically be implemented in the short term. In this policy paper, we show that many of the needs identified can in fact be financed without amending the Basic Law, and thus be addressed in the short term: the debt brake already provides options to take on debt for productive expenditure as part of the cyclical component and financial transactions.

“Fossil Fuel to the Fire: Energy and Inflation in Europe” is a research paper with three main findings. First, fossil fuels were the main cause Europe’s recent inflation. Second, replacing fossil fuels with renewable energy can increase price stability. Third, the right policy are needed today to realise this potential in the future.

This paper traces the transformation of the monetary architecture and concomitant sovereign debt issuance practices in Prussia and the German Empire from 1740 to 1914 in order to reflect on contemporary ideas regarding the appropriate relation between states’ treasuries, central banks, and the private banking system in matters of sovereign debt issuance.

This paper studies the emergence of sovereign spreads in the Eurozone prior to the financial crisis. We find that the Eurosystem’s move from unconditional to conditional collateral eligibility of sovereign bonds in 2005 triggered the emergence of sovereign spreads in the Eurozone, becoming effective through a periphery premium.

Europe needs LNG imports to ensure energy security, but decisions taken now should not undermine the achievement of climate goals. This background paper presents facts and solutions for reconciling energy security and climate in LNG decisions.

Statement by Philippa Sigl-Glöckner at the European Parliamentary week 2023 – Plenary session: Review of the EU economic governance framework – exchange of views, at February 28th 2023.

Italy’s economic stagnation is a problem for both Italy and Europe. This paper summarises and evaluates its main explanations. The best account is not that Italy’s didn’t reform, but that it undertook the wrong reforms and stuck with them for too long.

In this paper, we show that the case law on the legality of bond purchases by Eurosystem central banks is based in part on the economic theory of monetarism and, in particular, on a 1981 paper by Thomas Sargent and Neil Wallace (“Some Unpleasant Monetarist Arithmetic”). But monetarism, already controversial in the 1970s and 1980s, is now outdated. The assumptions on which Sargent and Wallance built their argument were already partly inaccurate then; today it is generally accepted that they do not apply in reality. This scientific progress should be taken into account in the interpretation.

We therefore develop in this paper an updated, “non-monetarist interpretation” of Article 123 TFEU.

In the paper, we very briefly sketch out the reform proposal put forward by the EU-Commission and make five suggestions on how this could be developed further. The annex contains two short papers covering (1) the EU methodology for computing debt sustainability and (2) expenditure rules in practice drawing on the Dutch experience.

Introductory statement at the Committee on Economic and Monetary Affairs of the European Parliament Public Hearing by Philippa Sigl-Glöckner – On shrinking the public balance sheet and the use of debt sustainability analyses, at November 30th 2022.